Head into the new year with clear tasks in mind for your financial goals.

TAX BREAKS[1]

The tax law changed and you may not be aware of all the tax breaks you are eligible to receive. The standard deductions almost doubled for 2019 to $12,200 for individuals, $18,350 for heads of household, and $24,400 for married couples filing jointly and surviving spouses.[2]

While the large increase in the standard tax deduction will allow for many Americans to forgo the task of itemizing their deductions, there are still some ‘above-the-line’ deductions you may want to claim. Most of these have no income limits so everyone is able to claim them.

- Student Loan Interest: You can claim up to $2,500 a year in student-loan interest IF your income as a single person is under $65,000 a year or $135,000 as a married person. This can be claimed for you, your spouse, or a dependent.

- Business Expenses: A lot of the ability for employees to claim business expenses was eliminated. However, school teachers still can claim up to $250 a year with the Educator Expense Deduction.

- Funding a Health Savings Account (HSA): IF you have a high deductible health insurance policy (over $1,350 a year for individuals and $2,700 a year for family plans) you can claim your HSA contributions. Depending on your employer, you can either contribute pre-tax dollars directly from your payroll, or you can claim a deduction if you contributed with after-tax dollars. You can contribute up to $7,000 for a family in 2019 or $3,500 for an individual. You will have to file a Form 8889. Check with your HR department to make sure you know what are your eligible expenses.[3]

- Charitable Donations: There was an increase in the percentage limit for charitable cash donations to public charities increased from 50% to 60% in 2018 and will remain at 60% for 2019.[4]

RETIREMENT PLAN LIMITS

Retirement plan contributions are tax deductible. By putting money aside in an IRA, 403b, or 401k, you are saving for your future and also reducing your taxable income. And remember, you have until April 15, 2019 to make your 2018 plan contributions! [5]

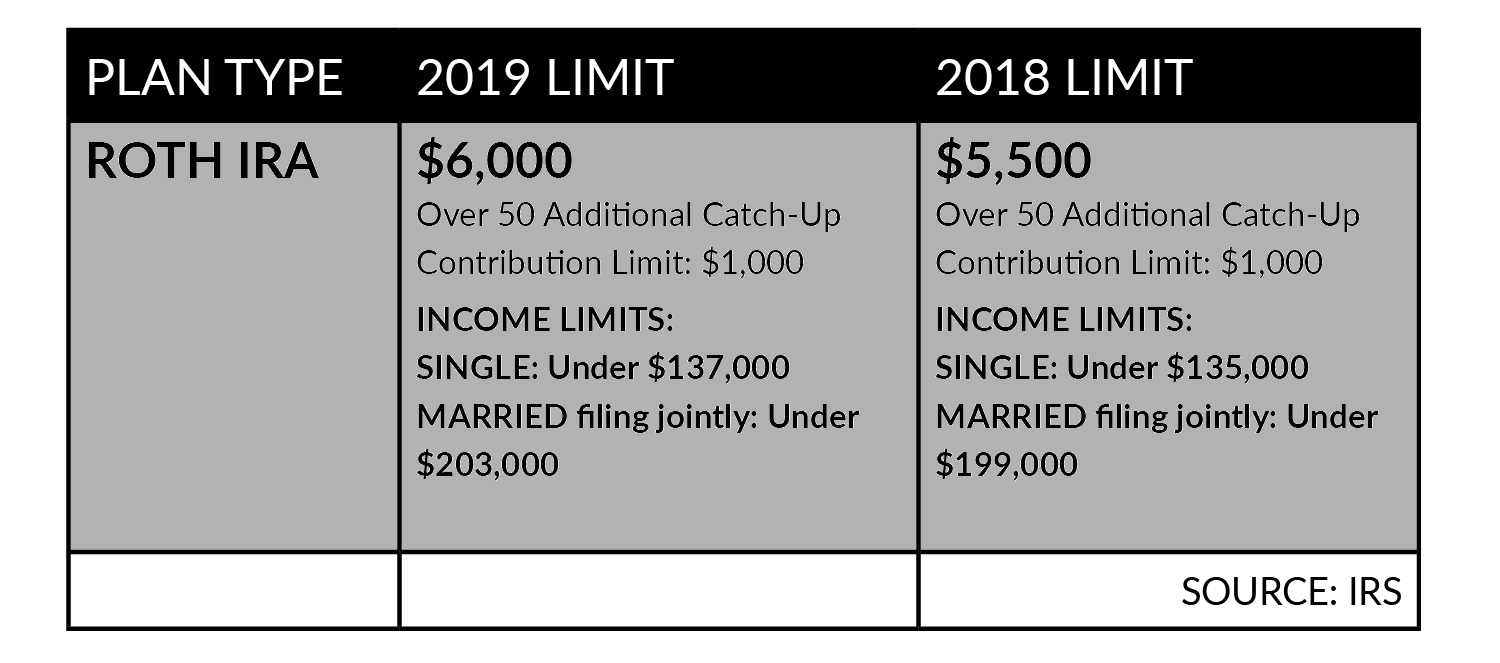

ROTH PLANS

For Roth accounts, you can only contribute to them if you make less than a certain amount of money. This salary amount was raised for 2019. Note that your contributions may be phased out at certain income levels so it is best to speak with your financial or tax advisor about your specific situation. [5]

CONTACT US with any retirement plan questions you have.

SOURCES:

[1] https://www.kiplinger.com/slideshow/taxes/T054-S001-tax-deductions-if-you-claim-the-standard-deduction/index.html

[2] https://www.forbes.com/sites/kellyphillipserb/2018/11/15/irs-announces-2019-tax-rates-standard-deduction-amounts-and-more/#1a8932572081

[3] https://www.kiplinger.com/article/insurance/T027-C001-S003-health-savings-account-limits-for-2019.html

[4] https://www.forbes.com/sites/kellyphillipserb/2017/12/20/what-your-itemized-deductions-on-schedule-a-will-look-like-after-tax-reform/#7e5e08ee6334

[5] https://www.irs.gov/newsroom/401k-contribution-limit-increases-to-19000-for-2019-ira-limit-increases-to-6000